- hello@daggloballtd.com

- No. 3 Ebong Close Wealth avenue, Palmsbay estate Abijo G.R.A. Lekki Epe exrpress way, Lagos State, Nigeria

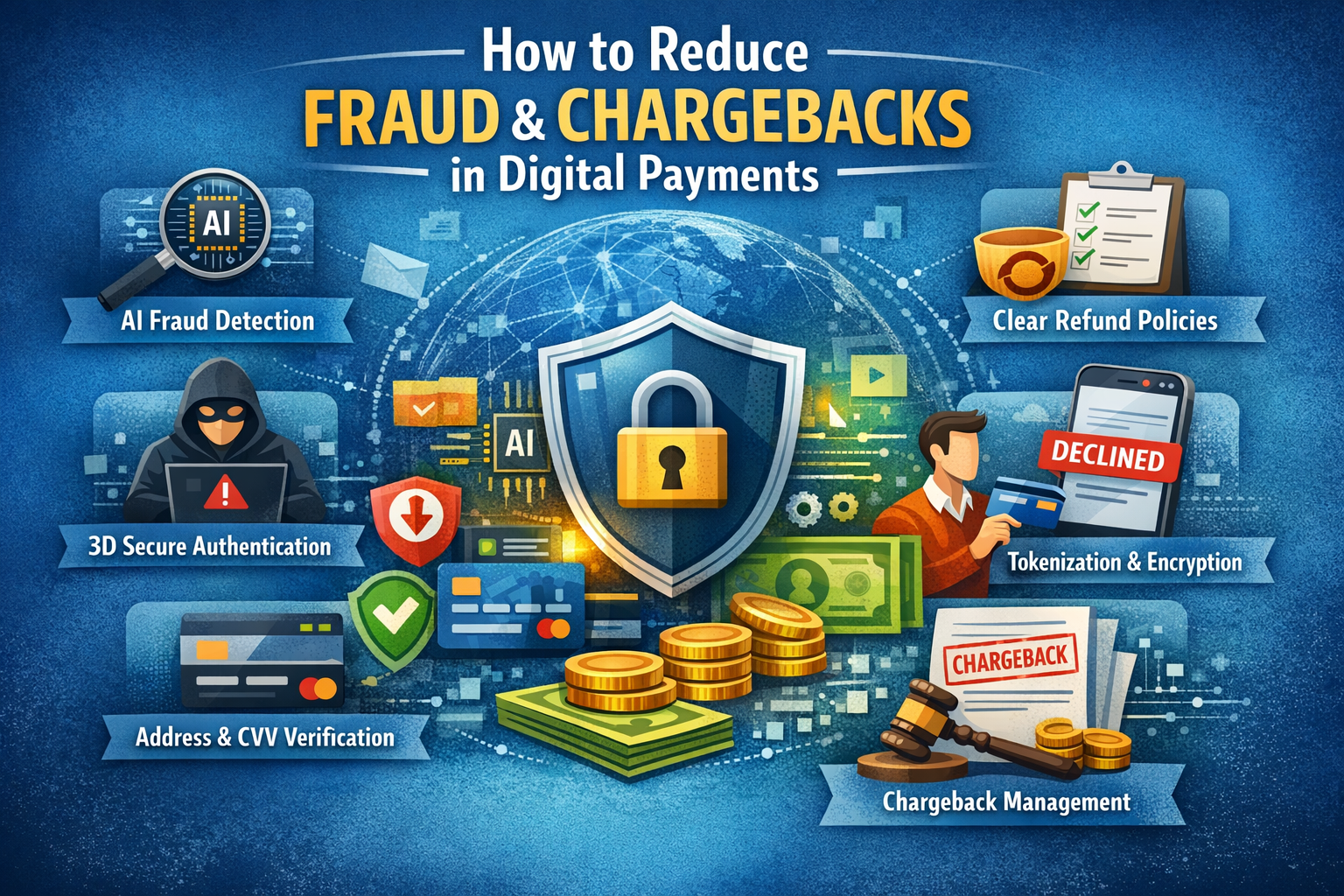

How to Reduce Fraud and Chargebacks in Digital Payments: 15 Proven Strategies to Protect Your Business

28

Feb

Digital payments have made business faster, borderless, and beautifully convenient. Customers can buy in seconds. Subscriptions renew automatically. Revenue flows while you sleep.

But here’s the uncomfortable truth: the same speed that fuels growth also fuels fraud.

Online payment fraud, friendly disputes, chargeback abuse they creep in quietly. One reversed transaction becomes ten. Ten become a pattern. And before you know it, your profit margins are bleeding.

So how do you scale confidently without opening the floodgates to risk?

This comprehensive guide answers the pressing question every digital business owner should be asking:

How to Reduce Fraud and Chargebacks in Digital Payments — without destroying customer experience?

Let’s break it down strategically.

Why Fraud and Chargebacks Are Draining Online Revenue

Fraud isn’t just a security issue. It’s a growth issue.

Chargebacks don’t just reverse a payment they add fees, damage your merchant reputation, and increase scrutiny from payment processors. Too many disputes? Your account could be flagged or even suspended.

Meanwhile, online payment fraud continues to evolve:

-

Card-not-present fraud is rising

-

Account takeovers are more sophisticated

-

Subscription confusion leads to avoidable disputes

-

Stolen credentials circulate on the dark web

The modern digital merchant must strike a delicate balance: frictionless checkout and airtight security.

And yes you can achieve both.

What Is Digital Payment Fraud?

Digital payment fraud refers to unauthorized or deceptive transactions conducted through online payment systems, often resulting in financial loss, chargebacks, and reputational damage for merchants.

Unlike physical retail fraud, online fraud thrives in anonymity. There’s no face, no signature, no physical card verification. It’s all digital and that makes security critical.

Common Types of Online Payment Fraud Businesses Must Watch

Understanding patterns helps you prevent them. Here are the most common types of online payment fraud:

-

Card-Not-Present (CNP) Fraud – Fraudsters use stolen card details for online purchases.

-

Account Takeover (ATO) – Hackers gain access to legitimate customer accounts.

-

Identity Theft – Stolen personal data used to create fraudulent transactions.

-

Friendly Fraud – Customers dispute legitimate purchases (intentionally or not).

-

Refund Fraud – Exploiting refund policies for free products or services.

-

Phishing Attacks – Deceptive emails or links capturing login credentials.

Each one contributes to chargebacks. And chargebacks? They’re expensive.

What Is a Chargeback in Digital Payments?

A chargeback is a payment reversal initiated by a cardholder’s bank after a transaction dispute, temporarily withdrawing funds from the merchant while the case is investigated.

Originally designed to protect consumers, chargebacks now create serious risk for merchants when abused.

Why Chargebacks Are Dangerous for Merchants

Chargebacks carry more weight than simple refunds.

They can:

-

Increase processing fees

-

Raise your chargeback ratio

-

Trigger fraud monitoring programs

-

Damage relationships with payment processors

-

Lead to merchant account termination

Most processors expect your chargeback ratio to remain below 1%. Exceed that threshold consistently, and you’re in trouble.

Now the real question becomes: How to Reduce Fraud and Chargebacks in Digital Payments before they escalate?

Let’s explore proven strategies.

How to Reduce Fraud and Chargebacks in Digital Payments (Step-by-Step Strategy)

1. Implement Strong Customer Authentication (SCA)

Strong Customer Authentication significantly reduces online payment fraud by verifying the identity of the buyer.

Use:

-

Two-Factor Authentication (2FA)

-

Multi-Factor Authentication (MFA)

-

3D Secure (3DS)

Modern 3D Secure systems intelligently apply authentication only when transactions appear risky — minimizing friction while maximizing security.

2. Use AI-Powered Fraud Detection Tools

Manual review can’t compete with automated fraud prevention.

AI-powered fraud detection tools use:

-

Machine learning algorithms

-

Behavioral analytics

-

Device fingerprinting

-

Real-time risk scoring

These systems analyze transaction patterns instantly and flag suspicious activity before it becomes a chargeback.

If you’re serious about digital transaction security, automation isn’t optional.

3. Enable Address Verification System (AVS) and CVV Checks

AVS fraud protection compares billing address details with bank records. If they don’t match, the transaction is flagged.

Pair that with mandatory CVV verification, and you add another protective layer.

Simple measures. Significant impact.

4. Use Tokenization and PCI DSS-Compliant Payment Security

Never store raw card details.

Instead, use:

-

Tokenization (replacing sensitive data with secure tokens)

-

End-to-end encryption

-

PCI DSS compliant payment gateways

PCI DSS compliance isn’t just a regulatory checkbox. It’s foundational to preventing online payment fraud.

5. Set Smart Transaction Limits and Risk Filters

Sometimes prevention is about boundaries.

Consider:

-

Limiting unusually high-value transactions

-

Blocking high-risk geographies

-

Monitoring multiple rapid purchases

-

Reviewing large first-time customer orders

Fraudsters often test small transactions before escalating. Catch the pattern early.

How to Reduce Fraud and Chargebacks in Digital Payments Through Better Customer Experience

Here’s something overlooked: not all chargebacks are fraud.

Many happen because customers are confused.

Clear Refund and Return Policies

Unclear policies create frustration. Frustration leads to disputes.

Make your refund policy:

-

Easy to find

-

Written in plain language

-

Transparent about timelines

-

Fair and consistent

Clarity prevents escalation.

Optimize Billing Descriptors

If your brand name doesn’t appear clearly on a bank statement, customers may assume fraud.

Use recognizable billing descriptors that match your business name.

A small tweak. Big difference.

Offer Proactive Customer Support

If customers can reach you quickly, they’re less likely to call their bank.

Provide:

-

Live chat

-

Fast email responses

-

Clear support channels

-

Quick refunds when appropriate

Sometimes it’s cheaper to refund immediately than to fight a chargeback.

Improve Subscription Transparency

Recurring billing is a major cause of friendly fraud.

Reduce disputes by:

-

Sending renewal reminders

-

Offering easy cancellation options

-

Avoiding hidden terms

-

Clearly explaining trial periods

Trust builds loyalty. Loyalty reduces disputes.

Chargeback Management Strategies: How to Handle Disputes Effectively

Even with strong fraud prevention, disputes may happen.

Understand the Representment Process

Representment allows you to submit evidence proving a transaction was legitimate.

Strong evidence includes:

-

Proof of authorization

-

Delivery confirmation

-

IP address logs

-

Customer communication records

-

Accepted terms and conditions

However, not every chargeback is worth fighting. Evaluate cost vs recovery.

Best Fraud Prevention Tools for Ecommerce and Digital Businesses

Several platforms provide built-in fraud detection and chargeback prevention:

-

Stripe Radar

-

PayPal Seller Protection

-

FraudLabs Pro

-

Riskified

-

Kount

Choosing the right fraud detection tool depends on transaction volume, business model, and risk tolerance.

Key Metrics to Monitor for Fraud and Chargeback Reduction

You can’t manage what you don’t measure.

Track these consistently:

-

Chargeback Ratio (keep below 1%)

-

Fraud Rate

-

Refund Rate

-

Approval Rate

-

False Decline Rate

These metrics reveal weaknesses before they become crises.

Future Trends in Digital Payment Fraud Prevention

The future of digital payment security is smarter and more predictive.

Emerging trends include:

-

Behavioral biometrics

-

AI-driven predictive fraud analytics

-

Real-time transaction monitoring

-

Zero-trust security models

Fraud prevention is evolving and businesses must evolve with it.

FAQs: How to Reduce Fraud and Chargebacks in Digital Payments

How can ecommerce businesses reduce chargebacks?

Ecommerce businesses can reduce chargebacks by implementing strong customer authentication, using fraud detection tools, maintaining transparent refund policies, and monitoring high-risk transactions.

What is the best way to prevent online payment fraud?

The most effective approach combines AI-powered fraud detection, 3D Secure authentication, AVS verification, and PCI DSS-compliant encryption.

Does 3D Secure reduce fraud?

Yes. 3D Secure adds an authentication layer that significantly reduces card-not-present fraud without severely impacting conversion rates.

What is considered a high chargeback ratio?

A chargeback ratio above 1% is typically considered high and may result in increased monitoring or penalties from payment processors.

Are chargebacks always caused by fraud?

No. Many chargebacks result from customer confusion, forgotten subscriptions, unclear billing descriptors, or delayed delivery.

Conclusion: Secure Payments Build Sustainable Growth

Learning how to reduce fraud and chargebacks in digital payments isn’t about building walls so high that customers feel unwelcome. It’s about building intelligent systems ones that recognize trusted customers while blocking suspicious activity.

When you combine:

-

Strong authentication

-

AI-powered fraud detection

-

Transparent communication

-

Clear policies

-

Proactive support

-

Continuous monitoring

You don’t just protect revenue you protect reputation.

And in the digital economy, reputation is everything.

Secure payments aren’t optional anymore. They’re the foundation of sustainable online growth.

Protect the transaction. Strengthen trust. Scale with confidence.